![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_gold.gif)

![[Most Recent Quotes from www.kitco.com]](http://www.kitconet.com/images/live/s_silv.gif)

Follow Up Re: Housing Bubble

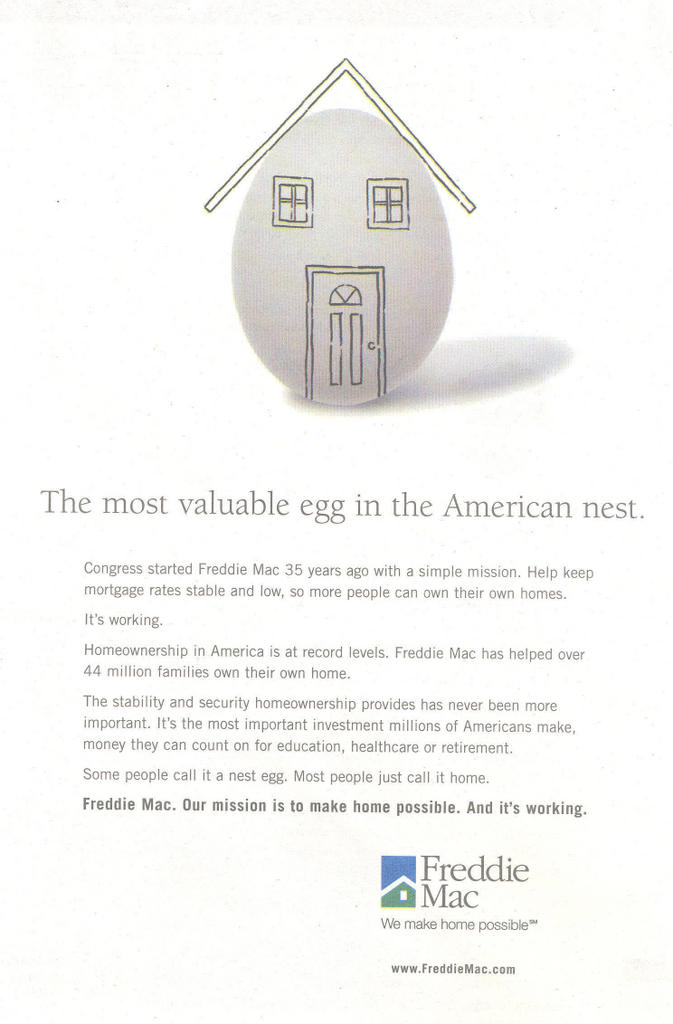

Just yesterday in this week's Barron's, I read an advertisement from Freddie Mac, that both disturbed and shocked me. It scared me first - that I might not really be in tune with the way that things work this day in age, or that maybe - it is everyone else - I don't know. Here is a copy of the advertisement:

The sentence that really got to me was: "It's the most important investment millions of Americans make, money they can count on for education, healthcare or retirement." You know it's funny, but I thought that Americans paid for their healthcare through their jobs or Medicare - not by taking out additional debt on their home. Furthermore, I thought that Americans paid for school by taking out student loans, applying for scholarships, or working an extra job, but apparently not - they do so by taking out another home loan. Finally, I thought that American paid for retirement by SAVING for retirement through a 401(k), pension plan, or investments. Apparently, I am severely mistaken, as Americans are being encouraged, even congratulated in this advertisement from the Federal Government (give me a break - Freddie Mac is basically a Government agency) - for taking on additional debt in order to tap their equity.

Just the other day, I overheard someone discussing home equity and how you know - when you start out you have nothing - but you have to get in that home right away to start building equity. You see according to this individual - equity was something that you earned - but you could only have access to that extra money by buying and living in the home. It resulted directly from your home price increasing. I mean shit - everyone knows that home prices in California only go up. You can't get hurt with dirt, etc. and so on. It's strange because I always thought that home equity resulted from paying down your mortgage.....

I think that far few people today understand the fundamental difference between home equity and savings. I think the real distinction is liquidity and perhaps most importantly risk. Savings is hard earned cash dollars that have been stashed away. The only risk that those dollars are not worth something is inflation - the idea that your dollars might buy less tomorrow than they do today. Savers are typically compensated for this risk though if they put their money in the bank by receiving interest on those funds.

Now lets contrast that with home equity, which is an amount that is impliedly tied to the price of an asset - your home. Now this home price is in fact a commodity which may fluctuate wildly in price, contingent on the amount of credit available in the country and the strength of the economy. Granted we have seen home prices in many areas of California triple over the past 5 years. The problem is that many buyers are not those who started in 2000 - many are buyers who obtained 100% financing and purchased within the last two years. These are individuals and families who are new to the game and may not fully comprehend what happens when your home is worth less than the amount you have borrowed. At that point you have what is called negative equity. This is not a fun concept.

As a nice follow up - check out this article at EuroPacific Capital from Peter Schiff who makes some great points on this very subject. This is a great wake up call. (www.europac.net) - read the 8/25/2005 post.

I guess the best retort to everything that I have posted here is that I am 25 years old and still live with my parents. My hopes of home ownership are slim to none in the current environment as my income could justify the purchase of a $150,000 home - not a $750,000 one. Unfortunately condos in San Diego go for $450,000 - so go figure.

-BG

posted by Ben Green @ 2:05 PM

![]()

![]()

0 Comments:

Post a Comment

<< Home